Great Rates - Better Service!

Mortgages

Whether it’s downtown trendy or spacious suburban, you decide. Our friendly lenders are here to help you make it a reality.

View Our Rates

*APR = Annual Percentage Rate. (Rates are "as low as")

**APY = Annual Percentage YIELD. (Rates are "as HIGH as")

Apply Online

Forget the paper. We brought the application process to you.

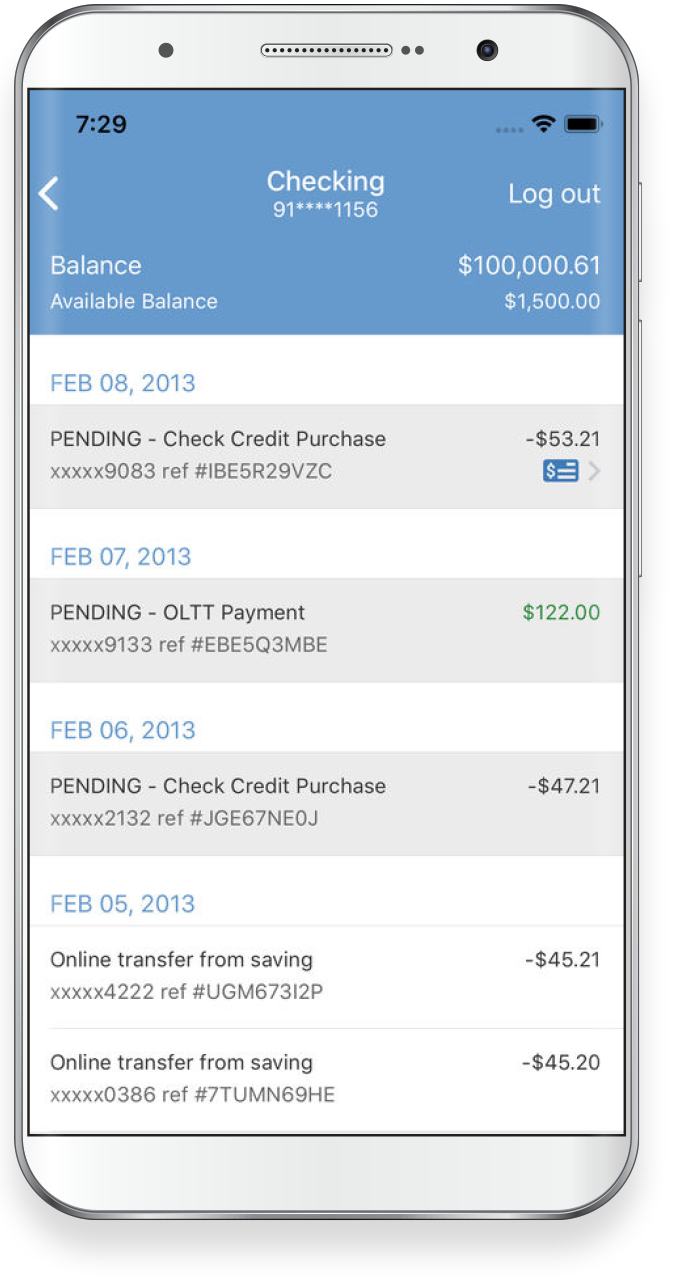

Available when you need us...

...doesn't matter where. Our account services fit around your schedule, anywhere life takes you.

Become a member

See the perks you’ll enjoy as a member — not a customer.

Are we your Credit Union?

Find out if you are a part of our select employer group.

I’ve been a member since 2000 and wouldn’t go anywhere else! Thank you Tremont!